Updated July 25, 2025

Climate-related risks abound for businesses today, including supply chain disruptions, storm-related flooding, regional droughts and wildfires, and increasing disclosure requirements. However, responding strategically to these challenges also creates opportunities for innovative businesses to increase efficiencies, boost revenue, improve organizational and community resilience, enhance brand value and raise employee engagement.

In 2024, MSCI found that annual returns from climate risk leaders on their All Country World Index (ACWI) outperformed those of laggards by 2-3% annually over the last 10 years. Whether companies are just starting their climate disclosure journey or are adapting existing reports to comply with new standards, companies can create lasting value by assessing their climate-related risks and opportunities and innovating to move beyond compliance.

In the US, California is working toward comprehensive, comparable and clear climate disclosures, with the reporting deadlines for the California Corporate Climate Disclosure laws (Senate Bills 253 and 261) fast approaching. California’s economy is the fourth-largest in the world, having surpassed Japan in March. Therefore, it’s essential that investors, regulators and stakeholders understand businesses’ climate-related risks, to assess progress toward a resilient economy. Effective disclosures also provide a meaningful pathway for businesses to reduce risk and increase resilience for the long-haul. To unlock the full potential of climate disclosures, companies should thoughtfully apply their physical and transition risk assessments to improve organizational and community resilience.

What is California’s Corporate Climate Disclosure Package?

In October 2023, California passed two laws requiring increased climate-related reporting from large companies with economic activities in the state, starting in 2026. The first law, Senate Bill (SB) 253, requires that companies “doing business in California” with over $1 billion in annual revenue publicly disclose their greenhouse gas (GHG) emissions and obtain assurance on the disclosures, with a nonfiling penalty of $500,000 per year.

Specifically, SB253 requires Scope 1 and 2 disclosures starting in 2026 for 2025 emissions (with limited assurance in 2026 phasing to reasonable assurance in 2030) and Scope 3 emissions disclosures starting in 2027 for 2026 data, with limited assurance beginning in 2030. For organizations unfamiliar with the scopes, Scope 1 emissions are controlled by the reporting entity, while Scope 2 emissions are controlled by upstream power producers and Scope 3 emissions are controlled by both upstream and downstream entities, according to the category.

Emitting activities reported under Scope 1, 2 and 3 emissions

The second law, SB 261, tackles climate-related risks and opportunities, requiring that companies “doing business in California” with over $500 million in annual revenue publish a climate-related financial risk disclosure by January 1, 2026 that is aligned with the recommendations of the Task Force on Climate-Related Financial Disclosures (TCFD) “or any successor thereto,” with biennial disclosures after 2026 and a non-compliance penalty of $50,000 in each reporting year. The TCFD provides a framework for companies to conduct a climate scenario analysis, assessing the physical risks and transition risks and opportunities across their value chain, using the following categories.

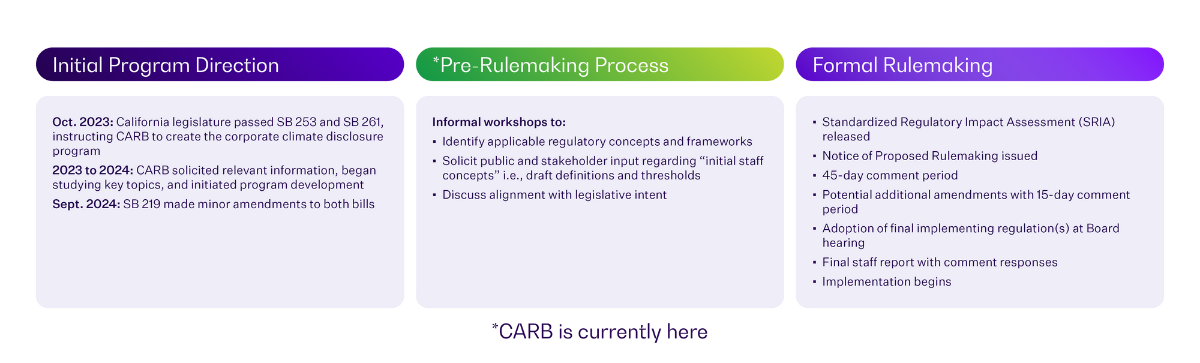

Since the bills passed, the California Air Resources Board (CARB) has been working to craft “implementing regulations” outlining exactly who is in-scope and how businesses will need to calculate emissions and assess climate-related risks. In September 2024, a third bill, SB 219, clarified some administrative requirements in the original two bills and extended the timeline for CARB to publish its implementing regulations.

These three bills—together, the Corporate Climate Disclosure Package—represent a step-change in sustainability reporting in the US, requiring comprehensive and comparable disclosures by the largest companies doing business in California.

Who Will Have to Report Under the Laws?

Since the bills’ passage, many companies have wondered, what counts as “doing business in California?” And which frameworks or protocols should be used to comply with the laws? These questions will be answered definitively when CARB finalizes their implementing regulation(s)— expected by the end of 2025. In the meantime, TRC’s practitioners experienced in climate risk, resilience and sustainability advisory services are closely monitoring CARB’s progress to keep our clients informed of upcoming regulatory requirements.

On May 29, 2025, CARB held a workshop announcing their intended definitions of key terms and compliance requirements (called “initial staff concepts”). This workshop was part of CARB’s “pre-rulemaking” informal stakeholder engagement. Once CARB issues a “Notice of Proposed Rulemaking,” there will be a 45-day formal comment period, a possible amendment phase and then final regulation adoption before the end of the year.

During the workshop, CARB announced several draft definitions affecting which entities are in-scope, as follows:

- Parent and subsidiary relationships to be defined based on ≥50% operational control

- “Annual revenue” to be defined as “gross receipts,” as specified in CA’s Revenue and Taxation Code section 25120(f)(2)

- “Doing business in California” to be defined as in the Tax Code Section 23101 with the following slight modification, that companies would be in-scope if they meet the law’s revenue threshold and meet any of these four criteria:

- Organized or commercially domiciled in California

- Have $735,019+ of sales in CA, inflation-adjusted in future years OR >25% of total sales

- Have $73,502+ of total real and tangible property in CA OR >25% of total property in state

- Have $73,502+ payroll compensation in state OR >25% of total payroll in CA

Based on workshop feedback, CARB may consider a higher monetary threshold for the payroll criteria above.

What Will Compliance Entail?

CARB also announced which protocols are likely to be required for compliant disclosures.

For SB253, CARB will likely specify that companies utilize the GHG Protocol, the leading emissions calculation framework used internationally. However, CARB regulations must meet strict clarity and specificity standards (by state law), meaning that CARB will likely have to layer additional specific disclosure requirements onto the GHG Protocol to clarify certain provisions. Recognizing that the timeline would be tight for entities to comply with CARB’s final regulations (to be published in late 2025) for the first Scope 1 and 2 disclosures in 2026, CARB published an enforcement notice in December 2024, stating that the agency will not levy fines for partial emissions data reported in 2026, as long as companies make a “good faith effort” to comply, using data that they already possess. The agency emphasized that companies should use the remainder of 2025 to improve their data collection systems and data completeness for future reporting cycles.

For SB261, CARB will create a public docket for all covered entities to provide a link to their published climate-related financial risk report. This docket will be open from December 1, 2025 to July 1, 2026. CARB also clarified that disclosures made in the first reporting cycle (ie. by the statutory deadline of January 1, 2026) may use data from fiscal years 2023–2024 or 2024–2025, according to the company’s “best available information.”

CARB is seeking to enable interoperability with existing climate disclosure requirements as much as possible, such as mandatory TCFD reporting in many countries and the European Union’s Corporate Sustainability Reporting Directive (CSRD). At the workshop, CARB announced that companies will likely need to implement “IFRS S2”, the International Financial Reporting Standards (IFRS)’s climate disclosure standard, which is the successor to the TCFD framework that will be updated as needed by the International Sustainability Standards Board (ISSB). The IFRS S2 fulfills all TCFD recommendations and enhances useability by clarifying specific required disclosures.

CARB recognized that it may take some time for companies to evolve their climate risk reporting from baseline TCFD alignment to full IFRS S2 compliance. Although CARB has not published an SB261 enforcement notice similar to that previously described for SB253, the agency noted during the workshop that they are likely to similarly recognize “good faith efforts” to publish a TCFD-aligned disclosure by January 1, 2026, without levying fines in this first reporting cycle, as companies work toward IFRS S2 compliance in future years. To prepare for IFRS S2, companies should conduct a quantitative climate scenario analysis, assessing the potential financial impacts of their physical and transition-related risks.

Key Disclosures Included in IFRS S2 Compliance vs. TCFD Recommendations

Note that IFRS S2 compliance requires disclosure of Scope 1, 2 and 3 emissions, in accordance with the GHG Protocol. Therefore, if CARB proceeds with its current draft definitions, companies with revenues over $500 million but below $1 billion would still need to report their GHG emissions in their SB261-compliant climate risk report, although they would not need to obtain assurance on their emissions disclosures, since they are out-of-scope for SB253. The details of eligibility for companies in this revenue bracket may change once CARB finalizes their implementing regulations.

Start Preparing Now: Three Key Recommendations

Adapting to a new regulatory framework can be overwhelming, but there are steps businesses can take today to prepare.

- Assess where you’re at, in terms of climate emissions data, risk management systems and climate risk reporting. Maybe you have yet to report your Scope 3 emissions or are working to integrate climate-related risks into your Enterprise Risk Management (ERM). Perhaps you’ve published sustainability reports in the past but have not yet aligned to the TCFD recommendations. Developing a baseline and knowing where you are starting from—across each of the disclosure areas—is key.

- Make a plan for future reporting cycles. Where are you prepared to meet California’s upcoming requirements, and which areas will require more effort? If you’re already disclosing Scope 1 and 2 emissions, you may want to conduct an assurance-readiness audit of your inventory and build time into the 2026 reporting cycle to acquire limited assurance on your 2025 data. You may consider conducting a Scope 3 emissions data gap assessment, to prepare for 2027 disclosures. If you’ve done a qualitative scenario analysis, perhaps it’s time for a more rigorous, quantitative dive into your physical risks. Or maybe your organization has a full TCFD-aligned report ready for the January 1, 2026, deadline, but you need to learn more about how to comply with IFRS S2 by the 2027 cycle.

- Work internally to get the ball rolling. Based on your assessment of where effort is needed, start to get buy-in from key decision-makers, assess budgets and data gaps, set goals and form relevant committees. These steps all take time, so start as soon as possible. There are many useful actions that organizations can take throughout 2025, while CARB is working to finalize the implementing regulations.

TRC Can Help You Create Value Through Disclosures

TRC’s tested practitioners have extensive experience helping companies adapt to evolving climate regulations with insightful and carefully crafted analysis that creates value far beyond compliance. Our solutions can help you uncover efficiencies, streamline processes, improve brand loyalty and recover more quickly from climate-related challenges.

Our specialists provide case-by-case advice to meet you where you’re at, crafting a customized emissions inventory approach and a bespoke climate scenario analysis, tailored to the material impacts you care about. We understand the nuances of regulatory compliance and are grounded in business realities, while helping you unlock the full value of climate risk assessment. Our emissions and climate resilience practitioners work seamlessly together, to assess and level up your GHG inventory and climate risk analysis.

Reach out today to jumpstart your organization’s climate disclosure improvements.